Understanding unsubsidized loans can be challenging, especially when it comes to deciphering the various aspects of interest accrual and repayment. This guide will walk you through the essential details of unsubsidized loans, offering practical advice and actionable steps. We’ll address common concerns and provide clear solutions to help you make informed decisions.

Understanding Unsubsidized Loans

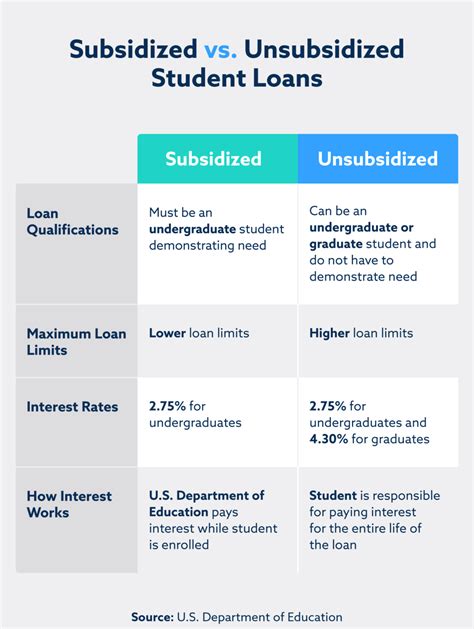

Unsubsidized loans are a type of federal student loan provided by the U.S. Department of Education. Unlike subsidized loans, where the government pays the interest while you're in school, interest on unsubsidized loans accrues from the time the loan is disbursed. Here's what you need to know to better manage your unsubsidized loans:

Immediate Action Item

One of the first steps to manage your unsubsidized loan is to start tracking the interest as soon as you receive the loan. Monitoring the interest can help you better plan your repayment strategy and potentially save you money over time.

Essential Tip

To avoid accruing too much interest, consider making payments while you're still in school. Even small payments can help reduce the overall amount you'll owe when you graduate and start repaying your loan in full.

Common Mistake to Avoid

A common mistake is underestimating the impact of interest accrual on your loan balance. Failing to make regular payments can lead to significant interest accumulation, making your loan balance grow faster than expected.

Quick Reference

- Immediate action item: Track your interest as soon as the loan is disbursed.

- Essential tip: Make payments while in school to reduce overall interest.

- Common mistake to avoid: Don’t underestimate the impact of interest accrual.

Managing Interest on Unsubsidized Loans

Managing interest on your unsubsidized loan requires proactive steps. Here's how you can handle it effectively:

When you first receive a unsubsidized loan, it’s important to understand how interest begins to accumulate. Here’s a step-by-step guide:

- Know When Interest Begins: Interest starts accruing from the date the loan is disbursed. This is when you should start making note of the interest.

- Monitor Your Loan Details: Regularly check your loan balance and the accrued interest. Most student loan servicers provide this information through their website.

- Make Minimum Payments: Even small, minimum payments can help reduce the overall amount of interest that will accrue when you’re fully responsible for repayment.

- Consider Income-Driven Repayment Plans: If you’re struggling to repay your loan, consider enrolling in an income-driven repayment plan. These plans cap your monthly payments based on your income and family size.

- Stay Informed: Keep up with any changes in your loan terms and payment plans. Understanding your options is crucial for managing your loan effectively.

By taking these steps, you can significantly reduce the amount of interest you'll pay over the life of your loan.

Strategies for Reducing Interest on Unsubsidized Loans

Reducing interest on unsubsidized loans involves both short-term actions and long-term strategies:

Short-Term Actions

When you first receive your unsubsidized loan, the following short-term actions can help you manage interest:

- Review Loan Terms: Carefully review the terms of your loan, including interest rates and repayment periods.

- Make Partial Payments: As soon as you can afford, make small partial payments. These payments will help reduce the amount of interest that accrues.

- Set Up Automatic Payments: If your school offers a repayment plan, set up automatic payments to ensure you never miss a due date.

Long-Term Strategies

For long-term management of your loan, consider the following strategies:

- Graduate with Less Debt: Focus on completing your degree faster to shorten the repayment period.

- Refinance Your Loan: Explore refinancing options. Private lenders may offer better rates, which can reduce your overall interest costs.

- Consolidate Loans: If you have multiple unsubsidized loans, consolidating them into one loan with a lower interest rate can save you money.

Practical Tips for Loan Management

Here are some practical tips to help you manage your unsubsidized loan more effectively:

- Budget Wisely: Create a budget that includes your loan repayment. Track your expenses to ensure you can comfortably afford your payments.

- Build an Emergency Fund: Having a small emergency fund can prevent you from using your loan funds for unexpected expenses, which could lead to additional interest charges.

- Utilize Loan Forgiveness Programs: Research programs that offer loan forgiveness in exchange for public service or other employment. These can help eliminate a significant portion of your debt.

FAQs on Unsubsidized Loans

What happens if I don’t make any payments on my unsubsidized loan?

If you don’t make any payments, interest will continue to accrue, and the balance of your loan will grow. Eventually, the Department of Education may refer your loan to a debt collection agency. To avoid this, make at least minimum payments even if you can't pay in full.

Can I pay off my unsubsidized loan early?

Yes, you can pay off your unsubsidized loan early without incurring any prepayment penalties. Making extra payments can reduce the overall interest you’ll pay, but remember to spread payments evenly throughout the year to maintain interest savings.

How does repayment differ from subsidized loans?

With unsubsidized loans, interest accrues while you’re in school and on grace periods, whereas with subsidized loans, the government pays the interest while you’re in school. Additionally, unsubsidized loans typically have higher interest rates.

By understanding and implementing these strategies, you can effectively manage your unsubsidized loan and reduce the financial burden it places on your future. With proactive management, you can ensure that your loan becomes a stepping stone to your future rather than a financial setback.