Understanding the effective interest rate formula is crucial for anyone engaged in financial planning or investment analysis. The effective interest rate, also known as the effective annual rate (EAR), provides a clearer picture of the true cost of borrowing or the true return on investment when dealing with interest compounded at intervals other than once a year. This article delves into the practical applications of the effective interest rate formula, offering expert insights and real-world examples to enhance your comprehension.

Why the Effective Interest Rate Matters

The effective interest rate formula helps to standardize interest rates, allowing for more accurate comparisons between loans and investment products that compound interest at different frequencies. Without it, comparing an annual percentage rate (APR) that compounds monthly with one that compounds daily could be misleading. For example, a loan advertised at an APR of 5% compounded monthly might seem attractive, but applying the effective interest rate formula reveals that its true annual cost is slightly higher due to the effect of compounding.

Key Insights

Key Insights

- Primary insight with practical relevance: The effective interest rate formula provides a more accurate comparison between different borrowing or investment options.

- Technical consideration with clear application: Understanding and calculating EAR is essential when comparing the cost of different loans or returns on various investment products.

- Actionable recommendation: Always use the effective interest rate formula when evaluating financial products with varying compounding frequencies.

Breaking Down the Effective Interest Rate Formula

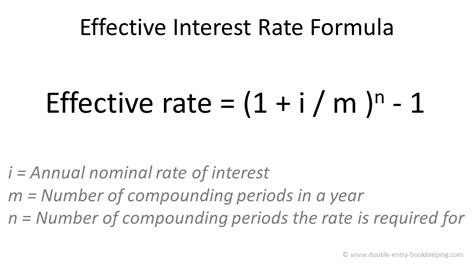

To understand the formula, it’s vital to first grasp its mathematical foundation. The effective interest rate formula is expressed as:

EAR = (1 + i/n)n - 1

Where i is the nominal annual interest rate, and n is the number of compounding periods per year. This formula adjusts the nominal rate to reflect the impact of compounding, providing the actual annual yield or cost. To make this more practical, consider a savings account with a nominal interest rate of 4% compounded quarterly. Applying the formula, we calculate:

EAR = (1 + 0.04/4)4 - 1 = 0.0406, or 4.06%

This result shows the true annual return, accounting for the effect of quarterly compounding.

Applications of the Effective Interest Rate Formula

The application of the effective interest rate formula extends beyond simple interest comparisons. In corporate finance, for instance, it plays a pivotal role in the valuation of loans and investments. Accurate calculations using the effective interest rate formula ensure that companies and investors make informed decisions.

Let’s consider a mortgage scenario. Suppose you have two mortgage options: one with a nominal annual interest rate of 5% compounded monthly and another at 4.8% compounded semi-annually. To decide which option is more cost-effective, you must apply the effective interest rate formula:

For the first mortgage: EAR = (1 + 0.05/12)12 - 1 = 0.0512, or 5.12%

For the second mortgage: EAR = (1 + 0.048/2)2 - 1 = 0.0492, or 4.92%

From this calculation, it becomes evident that the second mortgage has a lower effective annual cost, providing more savings over the loan term.

FAQ Section

What if the compounding period is more than once a year?

Even with more frequent compounding periods, you can use the effective interest rate formula to accurately determine the annual effective rate by adjusting the number of compounding periods in the formula.

Can the effective interest rate be greater than the nominal interest rate?

Yes, the effective interest rate can be greater than the nominal rate if compounding occurs more frequently than annually. This is because each compounding period applies interest on the previously accumulated interest.

Understanding the effective interest rate formula equips you with a vital tool for making precise financial comparisons and decisions. By employing this formula, you ensure that your evaluations account for the impact of compounding, leading to more accurate and informed financial planning.