In today’s competitive business landscape, companies must continually seek ways to reduce operational costs without sacrificing quality. Least Cost Theory provides a robust framework for understanding and achieving optimal cost efficiency. By focusing on the interplay between resource availability and cost structures, businesses can devise strategies that ensure they are not only minimizing expenses but also maximizing output and profitability. This article delves into the principles of Least Cost Theory and its practical application to modern business practices.

Key Insights

- Primary insight with practical relevance: Least Cost Theory helps businesses identify the most economical ways to produce goods or services.

- Technical consideration with clear application: Understanding the relative costs of various inputs allows firms to make informed decisions about resource allocation.

- Actionable recommendation: Implement cost analysis tools and regularly review resource usage to adopt Least Cost Theory effectively.

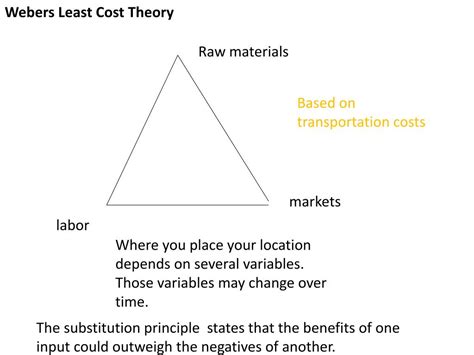

Fundamentals of Least Cost Theory

Least Cost Theory is rooted in the idea that firms seek to produce at the lowest possible cost by optimizing the combination of inputs. The primary goal is to align production processes with the most cost-effective resources, taking into account factors such as labor, raw materials, and technology. Historically, this theory has been pivotal in shaping production strategies in industries ranging from manufacturing to agriculture. It hinges on the notion that firms have flexible production technologies that enable them to vary their use of different inputs based on cost differentials. Understanding these cost dynamics allows businesses to adapt quickly to market changes and maintain competitive advantage.Application in Modern Business

In contemporary business settings, Least Cost Theory is more relevant than ever. The globalization of markets and advancements in technology have made input costs highly variable. Companies that can leverage this theory are better positioned to optimize their operations. For instance, a manufacturing firm might choose to source materials from regions where they are cheaper, without compromising quality, or might invest in automation technologies that reduce labor costs. Real-world applications include supply chain optimization, where companies meticulously analyze the cost-efficiency of their logistics networks. By adopting Least Cost Theory, businesses can significantly reduce overheads, drive down prices for consumers, and improve their bottom line.How can small businesses benefit from Least Cost Theory?

Small businesses can benefit by carefully analyzing their operational expenses and finding cost-saving measures without compromising service quality. Whether it’s negotiating with suppliers for better rates or streamlining internal processes, the application of Least Cost Theory can help them manage resources more efficiently.

What are common pitfalls when implementing Least Cost Theory?

One common pitfall is a failure to consider the long-term implications of short-term cost-cutting measures. Businesses may prioritize immediate savings over sustainable growth strategies, which can lead to inefficiencies in the future. Additionally, underestimating the value of quality and customer satisfaction in the cost equation can also be detrimental.

The application of Least Cost Theory is indispensable for businesses aiming to thrive in today’s economically challenging environment. By understanding and applying the principles of this theory, companies can achieve greater cost efficiency and ultimately secure their market position. Whether through meticulous cost analysis, leveraging technology, or strategic resource management, the insights derived from Least Cost Theory are essential for any forward-thinking business leader.