Are you overwhelmed with the myriad options available for loans, particularly struggling to decode the difference between Sub and Unsub loans? This comprehensive guide aims to unravel these complexities by providing step-by-step guidance with actionable advice and practical solutions, all while addressing the common pain points you may face as a user. By understanding the differences between Sub and Unsub loans, you’ll be better equipped to make informed decisions tailored to your financial situation.

Understanding the Basics

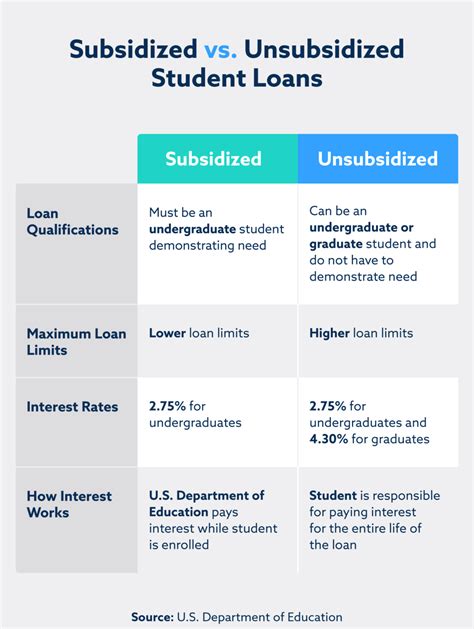

Let’s start by understanding the fundamental differences between Sub and Unsub loans.

A Sub (subordinate) loan is generally offered to individuals who have less-than-perfect credit or are new to borrowing. Banks or financial institutions are often more cautious with these loans, providing them through government-guaranteed or government-assisted programs. Unsub (unsubordinate) loans, on the other hand, are offered to individuals with good credit scores, providing better terms and lower interest rates.

Quick Reference

Quick Reference

- Immediate action item with clear benefit: Check your credit score to determine if you’re likely to qualify for an Unsub loan. If not, consider ways to improve your credit.

- Essential tip with step-by-step guidance: To improve your credit, start by paying all your bills on time, reducing your credit card balances, and avoiding new debt while improving.

- Common mistake to avoid with solution: Avoid shopping around for loans with multiple institutions in a short period. This can negatively impact your credit score; instead, do thorough research and apply only when ready.

How to Choose Between Sub and Unsub Loans

Selecting between Sub and Unsub loans can be a daunting process, but following these detailed steps can help simplify your decision-making process:

Step 1: Assess Your Credit Score

Your credit score is a primary determinant of whether you qualify for a Sub or Unsub loan. To start, pull your credit report from all three major credit bureaus (Experian, TransUnion, and Equifax) and review for any discrepancies or errors. If you find inaccuracies, dispute them immediately with the respective credit bureaus.

Step 2: Compare Loan Terms

Once you know your credit standing, compare loan terms offered by different institutions. Look for details such as:

- Interest rates

- Loan amounts

- Repayment duration

- Prepayment penalties

Use online comparison tools to visualize the differences and determine which loan offers the most favorable terms for your financial situation.

Step 3: Consider Government Programs

If you’re likely eligible for a Sub loan due to less-than-perfect credit, explore government-assisted loan programs. These often provide benefits such as lower interest rates and more flexible repayment options.

Step 4: Consult with a Financial Advisor

If the decision remains unclear, consulting with a financial advisor can offer personalized guidance tailored to your financial goals and current situation. Advisors can help you weigh the pros and cons of each loan type.

Detailed How-to for Applying for a Sub Loan

Applying for a Sub loan requires careful consideration to ensure you secure the best possible terms:

Step 1: Pre-Qualify with Multiple Institutions

Before you start the formal application process, pre-qualify with several lenders. This process is generally quick and doesn’t impact your credit score. It provides insight into the offers available to you.

Step 2: Gather Necessary Documentation

Collect all required documents before beginning the formal application. This typically includes:

- Proof of income (pay stubs, tax returns)

- Proof of identity (social security number, passport)

- Proof of residency (utility bills, rental agreement)

- Credit report

Organize these documents to make them easily accessible during your application process.

Step 3: Complete the Application Form

Fill out the loan application form accurately. Double-check all information for accuracy, especially details that pertain to your income, credit history, and personal identification. Any errors can lead to delays or denials.

Step 4: Submit a Solid Credit Appeal

If you’re seeking a Sub loan, be prepared to explain any negative marks on your credit report. Lenders often appreciate honesty and a genuine effort to improve your financial situation. Provide details of any past debts you’ve paid off or efforts you’ve made to rebuild your credit.

Step 5: Wait for Approval

Once your application is submitted, wait for the lender’s response. This can take a few days to a couple of weeks, depending on the lender’s review process.

Detailed How-to for Applying for an Unsub Loan

Applying for an Unsub loan is generally smoother due to better credit standings. Follow these steps to navigate the process:

Step 1: Verify Your Credit Standing

Ensure your credit report is error-free and up-to-date. You can request a free credit report from AnnualCreditReport.com once a year.

Step 2: Compare Loan Offers

Before applying, compare offers from different lenders. Use comparison websites to identify the most competitive rates and terms available to you.

Step 3: Compile Application Materials

Prepare the following documents to complete your application:

- Proof of income (recent pay stubs, recent bank statements)

- Credit report

- Identification (driver’s license, passport)

- Proof of residency (utility bill, lease agreement)

Step 4: Complete the Application Form

Fill out the loan application form accurately. Highlight any notable achievements or income sources to strengthen your application.

Step 5: Await the Approval

Lenders typically respond more quickly to Unsub loan applications due to the positive credit history. Be prepared for a faster turnaround time.

Practical FAQ

Common user question about practical application

What should I do if my Sub loan application is denied?

If your Sub loan application is denied, first review the lender’s explanation for the denial. Common reasons include insufficient income, high debt-to-income ratio, or unresolved negative credit marks. Here are steps you can take:

- Improve your credit score by making timely payments and reducing debt.

- Seek guidance from a financial advisor to understand your options.

- Wait a few months and reapply once your financial situation has improved.

In some cases, obtaining a credit co-signer with good credit can boost your chances of approval for a Sub loan.

Pro Tips and Best Practices

To navigate the world of Sub and Unsub loans more effectively, here are some additional tips:

- Start Small: If you’re new to borrowing, start with smaller loans to build your credit history gradually.

- Stay Informed: Keep up with changes in lending terms and interest rates to take advantage of the best offers.

- Maintain a Healthy Credit Utilization: Aim to keep your credit card balances below 30% of your credit limit.

- Review and Monitor: Regularly review your loan statements and credit report to ensure accuracy and identify any fraudulent activities.

By following this guide, you’ll have a clearer understanding of Sub and Unsub loans, making it easier to choose the option that best suits your financial needs. Armed with this knowledge, you can confidently approach the loan application process and secure the best possible terms for your financial future.