Understanding the tax multiplier formula is crucial for economists, policymakers, and businesses alike. The tax multiplier reveals how changes in government taxation policies can influence the overall economy. This comprehensive guide will demystify the tax multiplier formula through expert perspectives, evidence-based statements, and real-world examples, providing practical insights for application.

Key Insights

- The tax multiplier is a key economic concept that estimates the effect of tax changes on aggregate demand.

- It depends on the marginal propensity to consume (MPC), which affects how disposable income translates into consumption.

- Policymakers can use the tax multiplier to predict economic effects and guide fiscal policy.

Understanding the Core Concept

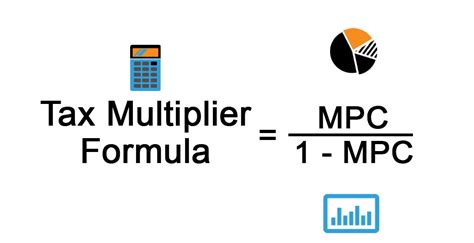

The tax multiplier formula is a fundamental tool for analyzing fiscal policy. At its core, it illustrates how changes in taxes impact total economic activity. The formula typically follows this structure:Tax Multiplier ™ = - (ΔY / ΔT) = - (1 / (1 - MPC))

Here, ΔY represents the change in aggregate output, and ΔT denotes the change in taxes. The negative sign indicates that an increase in taxes will lead to a decrease in economic output. This formula hinges on the marginal propensity to consume, a figure expressing the fraction of additional income that individuals are likely to spend. Understanding this formula requires a grasp of key economic principles and their practical applications.

Technical Considerations and Real-World Applications

A deep dive into technical considerations reveals the practical importance of the tax multiplier. For example, if the marginal propensity to consume is 0.8, the tax multiplier would be calculated as follows:TM = - (1 / (1 - 0.8)) = -5

This result implies that a 1 increase in taxes could potentially lead to a 5 decrease in economic output, demonstrating the powerful influence of fiscal policy on the economy. Real-world examples include government responses to economic downturns. During the 2008 financial crisis, several governments cut taxes to stimulate economic activity, utilizing the tax multiplier to predict the impact on aggregate demand.

The Tax Multiplier in Action: Case Studies

To illustrate the tax multiplier’s practical applications, consider the 2008 financial crisis. The U.S. government implemented the Economic Stimulus Act, including tax rebates designed to boost consumer spending. Using the tax multiplier, economists estimated that these rebates would positively affect aggregate demand and stimulate economic growth. While the exact outcome depended on various factors, the use of the tax multiplier provided a framework for policymakers to assess the potential benefits of fiscal stimulus.Another pertinent case study is the reduction of corporate taxes. For instance, in 2017, the U.S. Tax Cuts and Jobs Act reduced corporate tax rates significantly. Analysts utilized the tax multiplier to predict economic impacts, arguing that lower taxes could increase business investment and stimulate economic activity.

What is the difference between the tax multiplier and the fiscal multiplier?

The tax multiplier specifically measures the effect of changes in personal taxes on aggregate demand, whereas the fiscal multiplier encompasses all types of fiscal policy changes, including government spending and transfer payments. Both tools are essential for understanding economic dynamics.

How accurate is the tax multiplier in predicting economic outcomes?

The accuracy of the tax multiplier depends on several factors, including the marginal propensity to consume, which can vary due to economic conditions, consumer confidence, and external shocks. While it provides a useful estimate, actual outcomes may differ based on these dynamics.

In conclusion, the tax multiplier formula is an indispensable tool for understanding the interrelationship between taxation and economic activity. With a clear grasp of the formula and its practical applications, economists and policymakers can better navigate the complexities of fiscal policy, leading to more informed and effective economic decision-making.