I’ll create a blog post about the Thrift Savings Plan (TSP) following the specified guidelines:

The Thrift Savings Plan (TSP) is a powerful retirement savings vehicle that offers federal employees and uniformed service members a unique opportunity to secure their financial future. Designed similarly to 401(k) plans in the private sector, the TSP provides a structured approach to long-term wealth accumulation with several distinctive features that make it an attractive option for government workers.

Understanding the Thrift Savings Plan Basics

At its core, the TSP is a defined contribution plan that allows participants to invest a portion of their salary into a range of investment options. The plan offers significant advantages, including:

- Tax-deferred growth on contributions

- Potential employer matching contributions

- Low administrative costs

- Flexible investment strategies

Investment Options and Fund Choices

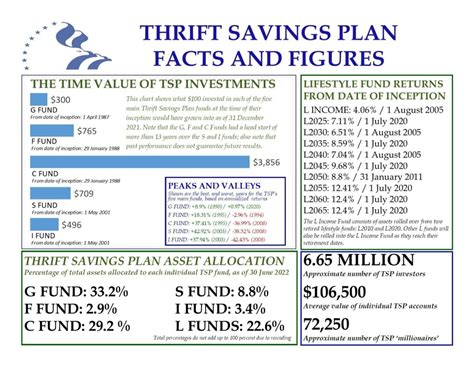

The TSP provides participants with a carefully curated selection of investment funds, known as the TSP core funds. These include:

| Fund Type | Description |

|---|---|

| G Fund | Government securities with low risk |

| F Fund | Fixed income index investment |

| C Fund | Common stock index investment |

| S Fund | Small to mid-sized company stocks |

| I Fund | International stock investment |

Contribution Strategies

Participants can maximize their TSP contributions through several strategic approaches:

- Regular payroll deductions

- Catch-up contributions for those over 50

- Automatic contribution increases

- Balancing between traditional and Roth TSP options

💡 Note: Always consider your individual financial situation when determining contribution levels.

Retirement Withdrawal Options

The TSP offers flexible withdrawal strategies that cater to different retirement needs. Participants can choose from various distribution methods, including:

- Partial withdrawals

- Systematic withdrawals

- Lifetime annuity options

- Lump-sum distributions

As federal employees navigate their retirement planning, the Thrift Savings Plan stands out as a robust and flexible tool for long-term financial security. By understanding its nuances and strategically managing contributions, participants can build a substantial nest egg for their future years.

How much can I contribute to TSP annually?

+

The annual contribution limit is adjusted yearly. For 2026, federal employees can contribute up to 23,000, with an additional 7,500 catch-up contribution for those 50 and older.

Can I roll over other retirement accounts into TSP?

+

Yes, you can roll over eligible retirement accounts like 401(k) plans from previous employers into your TSP account, subject to specific guidelines.

What is the difference between traditional and Roth TSP?

+

Traditional TSP contributions are made with pre-tax dollars, reducing current taxable income, while Roth TSP contributions are made with after-tax dollars, allowing tax-free withdrawals in retirement.