The advent of online education and e-learning platforms has significantly transformed the landscape of contemporary education, enabling a more expansive and diverse array of learners to access quality instruction from anywhere in the world. One term that has emerged within this ecosystem is “unsub loan,” a concept that may appear opaque to many, but holds immense practical significance. This article delves into the unsub loan mechanism, offering an expert perspective with actionable insights to ensure a comprehensive understanding.

Key Insights

- Unsub loans are a type of financial aid specifically designed to cover tuition and educational costs without the borrower having to make payments while enrolled in school.

- Technically, unsub loans differ from traditional federal student loans in that interest does not accrue while the student is in school, provided the student maintains satisfactory academic standing.

- A key action recommendation is to review personal financial goals and consult with a financial advisor to determine if an unsub loan is the right choice.

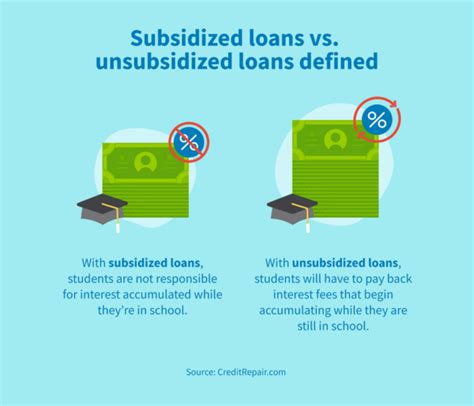

Unsub loans, often referred to as “unsubsidized loans,” represent a type of federal student loan that contrasts significantly with subsidized loans. Unlike their subsidized counterparts, which have interest payments covered by the government while the student is enrolled at least half-time, unsub loans accrue interest from the time the loan is issued. However, there’s a critical exception: while the student continues to maintain satisfactory academic status, the loan servicer will pause interest accrual.

This distinction plays a pivotal role in understanding how unsub loans work. For instance, when a student borrows an unsub loan and is deeply focused on their studies, they do not have to worry about interest accumulating on their loan. However, if academic performance drops, thus affecting their eligibility for this grace period, interest will start accruing immediately. This mechanic is instrumental for students who plan to take full advantage of the educational experience without financial interruptions.

In a practical scenario, let’s consider a hypothetical student named Alex, who plans to study engineering. During Alex’s enrollment, they decide to borrow an unsub loan to cover the rising tuition costs. Given Alex’s satisfactory academic performance, interest does not accrue on this loan until graduation. This ensures that Alex’s post-education financial planning does not get hampered by increasing debt prematurely. Upon graduation, Alex will then need to start repaying the loan, typically with a six-month grace period before full repayment begins, contingent upon Alex’s financial circumstances.

The primary technical consideration with unsub loans revolves around the interest accrual. While the grace period offers an advantageous reprieve, it’s crucial to monitor academic performance. Falling behind in studies can potentially lead to interest starting to accrue, thereby increasing the overall debt burden. Therefore, students should adopt diligent academic habits to ensure that the unsub loan benefits are fully realized without unexpected financial hits.

In the landscape of higher education financing, the unsub loan provides a critical tool for students seeking to manage their tuition expenses without immediate repayment obligations. It is vital for prospective borrowers to understand these mechanisms thoroughly. Here are a few frequently asked questions that further elucidate the nuances of unsub loans.

What happens if I drop below half-time enrollment?

If you drop below half-time enrollment, the grace period where interest does not accrue will end. Interest will begin to accrue on your unsub loan from the day your enrollment status changes, unless you make repayment or refinance the loan.

Can I consolidate my unsub loans with private loans?

Yes, you can consolidate your unsub loans with private student loans. However, it is advisable to consult with a financial advisor to understand the implications, as consolidation can affect your repayment terms and interest rates.

In summation, unsub loans provide an invaluable option for students navigating the complexities of higher education financing. By ensuring a clear grasp of how these loans work, students can optimize their financial strategies and secure their academic pursuits with less stress and greater confidence.